Which Global Regulations Are Shaping Cybersecurity in the Banking Industry?

You open your banking app to transfer money. You trust that your details are safe. But behind the scenes, a complex web of rules and standards works quietly to protect your data. These are not just suggestions. They are strict global regulations that banks must follow to operate. From New York to New Delhi, from London to Singapore, governments and financial authorities have created laws to fight cybercrime in banking. Why? Because one data breach can cost billions, ruin reputations, and shake public trust. In 2025, as cyber threats grow smarter, these regulations are evolving faster than ever. This blog explains the most important global rules shaping bank cybersecurity. We’ll use simple language, real examples, and clear comparisons so that anyone, from a student to a CEO, can understand what’s at stake and why it matters.

Table of Contents

- Introduction

- Why Cybersecurity Regulations Matter in Banking

- Key Global Regulations Shaping Banking Cybersecurity

- Comparison of Major Banking Cybersecurity Regulations

- Impact on Banks and Customers

- The Future of Banking Cybersecurity Regulations

- Conclusion

- Frequently Asked Questions

Why Cybersecurity Regulations Matter in Banking

Banks are not like regular companies. They hold your money, your identity, and your financial history. A single hack can lead to stolen funds, fake loans, or even national security risks. In 2024 alone, global banks lost over $12 billion to cyberattacks. Customers suffered. Economies wobbled. Governments stepped in.

Regulations do three big things:

- Force banks to build strong security systems

- Set clear rules for reporting breaches

- Punish banks that fail to protect customer data

Without rules, some banks might cut corners to save money. Regulations level the playing field. They protect you, even if your bank is small or new.

Key Global Regulations Shaping Banking Cybersecurity

Let’s look at the most important regulations from around the world. Each has unique rules, but all aim to make banking safer.

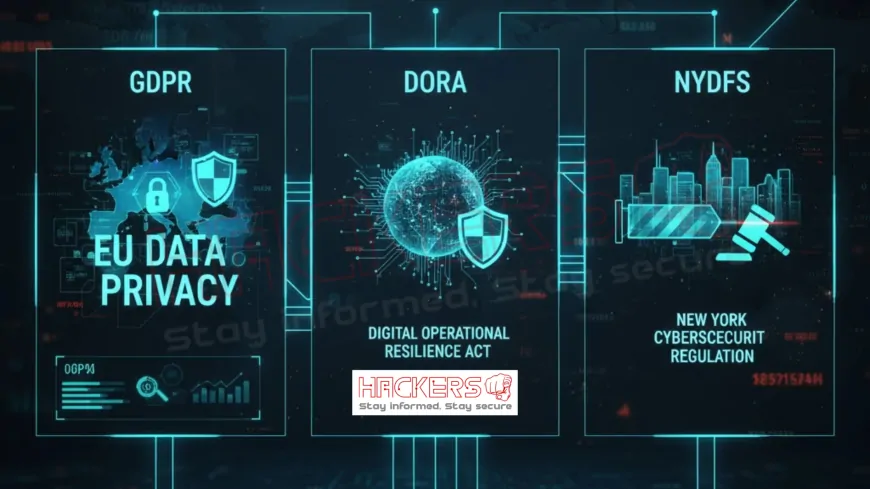

- GDPR (General Data Protection Regulation) - EU: Launched in 2018, GDPR is the gold standard for data privacy. It applies to any bank handling EU customer data, even if the bank is in India or the US. Banks must encrypt data, get clear consent, and report breaches within 72 hours. Fines can reach 4 percent of global revenue.

- NYDFS Cybersecurity Regulation - USA: The New York Department of Financial Services (NYDFS) introduced this in 2017. It applies to all banks operating in New York. Banks must appoint a Chief Information Security Officer (CISO), conduct annual penetration tests, and report cyber incidents within 72 hours.

- PSD2 (Payment Services Directive 2) - EU: This 2018 rule focuses on secure payments. It requires Strong Customer Authentication (SCA), meaning two-factor authentication (2FA) for online transactions. It also forces banks to share data securely with third-party apps via APIs.

- RBI Cybersecurity Framework - India: The Reserve Bank of India (RBI) issued guidelines in 2016 and updated them in 2023. Banks must have a cybersecurity policy, report incidents within 6 hours, and conduct regular audits. Public sector banks face extra scrutiny due to legacy systems.

- MAS Technology Risk Management - Singapore: The Monetary Authority of Singapore (MAS) requires banks to implement multi-factor authentication, encrypt sensitive data, and test systems regularly. It also mandates third-party risk assessments.

- CPNI and FCA Guidelines - UK: The UK’s Financial Conduct Authority (FCA) and Centre for the Protection of National Infrastructure (CPNI) require banks to follow operational resilience rules. Banks must identify critical functions and ensure they can recover from cyberattacks within hours.

- CCPA (California Consumer Privacy Act) - USA: Similar to GDPR, it gives California residents the right to know what data banks collect and delete it on request. Banks must disclose breaches and offer opt-out options.

- DORA (Digital Operational Resilience Act) - EU: Starting in 2025, DORA targets financial institutions. It requires stress testing, third-party risk management, and incident reporting across the EU.

These rules are not optional. Ignore them, and banks face massive fines, license loss, or jail time for executives.

Comparison of Major Banking Cybersecurity Regulations

Not all regulations are the same. Here’s a clear comparison:

| Regulation | Region | Breach Reporting Time | Requires CISO | Max Fine |

|---|---|---|---|---|

| GDPR | EU | 72 hours | No | 4% of global revenue |

| NYDFS | New York, USA | 72 hours | Yes | Varies by violation |

| RBI Framework | India | 6 hours | Yes (for large banks) | Up to ₹10 crore |

| MAS TRM | Singapore | Within 1 hour (critical) | Yes | Up to SGD 1 million |

| DORA | EU | 24 hours (initial) | Yes | Up to 1% of daily turnover |

As you see, India’s RBI demands the fastest reporting. The EU focuses on privacy and resilience. The US varies by state. Global banks must comply with all if they operate internationally.

Impact on Banks and Customers

Regulations change how banks work and how safe you feel.

For Banks:

- Hire more cybersecurity experts

- Invest in encryption, AI monitoring, and cloud security

- Train staff regularly

- Pay higher compliance costs: up to 10 percent of IT budget

- Face audits and stress tests

For Customers:

- Stronger passwords and 2FA become mandatory

- Faster alerts when something goes wrong

- Right to delete your data (in GDPR/CCPA regions)

- More trust in digital banking

Yes, compliance is expensive. But the cost of a breach is higher. In 2023, a major Indian bank paid ₹500 crore in fines and recovery after a data leak.

The Future of Banking Cybersecurity Regulations

By 2030, expect these trends:

- Global Standards: Bodies like the Financial Stability Board (FSB) may create unified rules.

- AI and Quantum Rules: New laws will cover AI risks and prepare for quantum computing that can break current encryption.

- Third-Party Focus: More scrutiny on vendors and fintech partners.

- Customer Rights: You may get a "cybersecurity score" for your bank, like a credit score.

- Real-Time Compliance: AI will monitor banks 24/7 and auto-report issues.

India is pushing for a national cybersecurity law. The EU plans DORA 2.0. The US may federalize state rules. Change is coming.

Conclusion

Cybersecurity in banking is no longer just about technology. It’s about rules, responsibility, and trust. From GDPR’s privacy hammer to RBI’s rapid reporting, global regulations are forcing banks to act. They demand CISOs, audits, encryption, and transparency. The cost is high, but the alternative is worse: lost money, lost faith, and lost future. For customers, these rules mean safer apps, faster alerts, and more control. For banks, they mean survival in a digital world. The message is clear. Comply, protect, and thrive. Or ignore, breach, and fall. In 2025 and beyond, regulations are not red tape. They are the shield between your money and the hackers trying to steal it.

Frequently Asked Questions

What is GDPR in banking?

GDPR is an EU law that protects personal data. Banks must secure it, get consent, and report breaches in 72 hours.

Does RBI have cybersecurity rules for banks?

Yes. RBI’s 2023 framework requires incident reporting in 6 hours, regular audits, and a cybersecurity policy.

What is a CISO?

A Chief Information Security Officer is a senior executive responsible for a bank’s cybersecurity strategy.

Why do banks need 2FA under PSD2?

PSD2 mandates Strong Customer Authentication to reduce fraud in online payments across the EU.

Can a bank be fined for a data breach?

Yes. GDPR fines can reach 4 percent of global revenue. NYDFS and RBI also impose heavy penalties.

Do Indian banks follow GDPR?

Only if they serve EU customers. But many adopt GDPR standards to attract global business.

What is DORA in the EU?

DORA is a 2025 law that ensures banks can withstand, respond to, and recover from cyber disruptions.

Are digital banks regulated differently?

No. They follow the same cybersecurity rules as traditional banks in their region.

What is third-party risk in regulations?

It means banks are responsible for the security of vendors they work with, like cloud or payment providers.

Can customers sue banks for weak security?

Yes, under GDPR or CCPA, if the bank was negligent and caused harm.

Why does Singapore have strict bank rules?

Singapore is a global finance hub. MAS ensures trust with tough cybersecurity and risk management laws.

Will regulations stop all bank hacks?

No, but they reduce risk, force quick response, and punish failure.

What is operational resilience?

It means a bank can keep running critical services even during a cyberattack or system failure.

Do all countries have banking cybersecurity laws?

Not yet. But major economies like the US, EU, India, and Singapore lead the way.

Can small banks afford compliance?

It’s challenging, but many use shared services, cloud tools, and government support programs.

What happens if a bank hides a breach?

Regulators impose bigger fines, ban executives, or revoke licenses. Transparency is mandatory.

Is encryption required by law?

Yes. GDPR, NYDFS, RBI, and MAS all mandate encryption for sensitive customer data.

Will there be a global banking cybersecurity law?

Not soon, but groups like the G20 and FSB are working toward common standards.

Do regulations cover mobile banking apps?

Yes. Apps must follow the same encryption, authentication, and testing rules as websites.

How often do banks get audited under these rules?

At least annually. High-risk banks face surprise checks and penetration tests.

What's Your Reaction?